CANADIAN NON-RESIDENT SELLING TO CANADA? IS IT TIME TO GET A GST/HST REGISTRATION

About the Goods and Services Tax/Harmonized Sales Tax

The goods and services tax (“GST”) applies to most supplies of goods and services in Canada. GST also applies to many supplies of real property (e.g., land, buildings, and interests in such property) as well as intangible personal property (e.g., trademarks, rights to use a patent, and digitized products downloaded from the Internet and paid for individually).

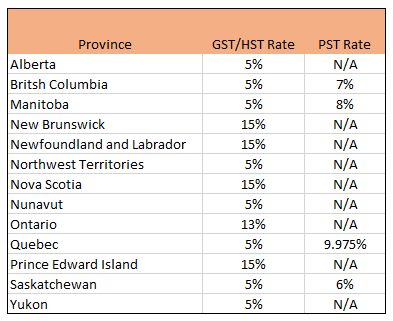

Between 1997 and 2013, six of Canada’s 10 provinces became “participating provinces” by harmonizing their provincial sales tax (“PST”) with the GST to implement the harmonized sales tax (“HST”). Generally, HST is applied to the same base of property ( i.e., tangible and intangible goods) and services as the GST. In some provinces, there are point-of-sale rebates equivalent to the provincial portion of the HST on certain qualifying items.

HST rates vary from one participating province to another as shown in the table below.

GST/HST registrants who make taxable supplies (other than zero-rated supplies) in the participating provinces, collect tax at the applicable HST rate. GST/HST registrants collect tax at the 5% GST rate on taxable supplies they make in the rest of Canada (other than zero-rated supplies).

Zero-rated supplies are still considered “taxable supplies” but are taxed at a rate of 0%.

Non-residents and GST/HST Registration

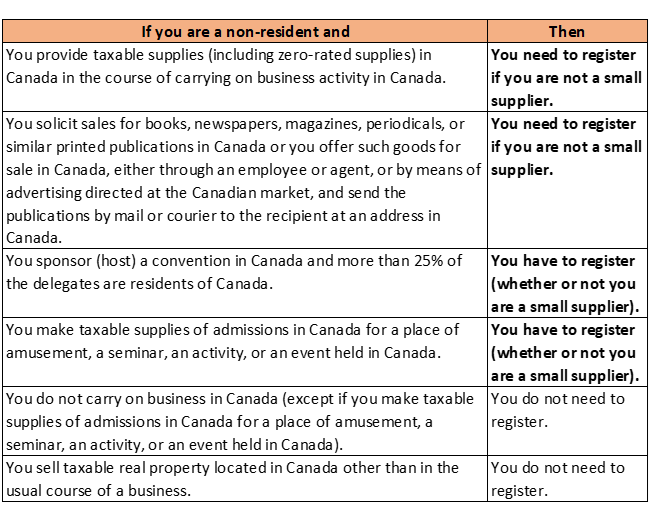

Even if you do not have a permanent establishment in Canada, you may be carrying on business in Canada. The following table can help you determine if you need to register.

Non-residents wanting to register for GST/HST must complete Form RC1, Request for a Business Number, and fax or mail it to their designated Canada Revenue Agency (“CRA”) non-resident tax services office.

*A small supplier refers to a person whose revenue (along with the revenue of all persons associated with that person) from worldwide taxable supplies (including zero-rated supplies) was equal to or less than $30,000 ($50,000 for public service bodies) in a calendar quarter and over the last four consecutive calendar quarters.

Charities and public institutions are also considered small suppliers if they meet the alternative gross revenue test of $250,000 or less.

Non-resident Security

If you do not have a permanent establishment in Canada, or if you make supplies in Canada through another person’s fixed place of business, and you apply to be registered for the GST/HST, you must provide the CRA with a security deposit.

The initial amount of the security is 50% of your estimated net tax (whether positive or negative) during the 12-month period after you register. For subsequent years, the amount of security is equal to 50% of your actual net tax for the previous 12-month period (whether positive or negative). The amount of security required will be adjusted by the CRA year over year and you will be notified of changes to the deposit requirements. If you estimate that you will supply taxable property and services in Canada of not more than $100,000 annually and your net tax will be between $3,000 remittable and $3,000 refundable annually, security is not required.

The maximum security deposit is $1 million and the minimum is $5,000. Security may be in the form of cash, certified cheque, money order, or a qualifying bond. The use of cash or cash equivalents (such as a certified cheque or a money order) may result in the cash being used to pay other outstanding debts to the CRA at the time the security is released. The CRA does not accept non-transferable bonds such as Canada Savings Bonds.

Input Tax Credits (ITC)

Once registered, you can reduce your HST remittances or recover GST/HST paid or payable on the expenses incurred or purchases made in the ordinary course of business. Such refundable taxes are known as Input Tax Credits or ITC. To be eligible for ITCs, the expenses must be necessary and reasonable.

ITCs must be claimed within a statutory timeline and be supported by source documents in case of a CRA audit or examination.